By Ben Malena 💥 CMO AlgoPear

For a decade, the biggest names in finance treated digital assets and embedded investing like a distraction. Vanguard dismissed it. Bank of America dragged its feet. Chase, Citi, U.S. Bank — all of them played defense.

But now? They’re sprinting.

Overnight, the same institutions that once mocked digital asset rails, retail investing apps, and real-time insights are rolling out their own versions — quietly, aggressively, and with the kind of force only trillion-dollar incumbents can apply.

And this is the part community FIs can’t afford to ignore:

When the slowest giants change direction, the rest of the industry follows — fast.

The adoption curve that used to take years is collapsing into months. What used to be “experimental” is becoming standard. And every credit union and community FI is about to feel the gravity of that shift in real time. Fintech started the trend. Consumers accelerated it. And now the largest banks in America are signaling that the new era of investing and digital asset services is not optional — it’s inevitable.

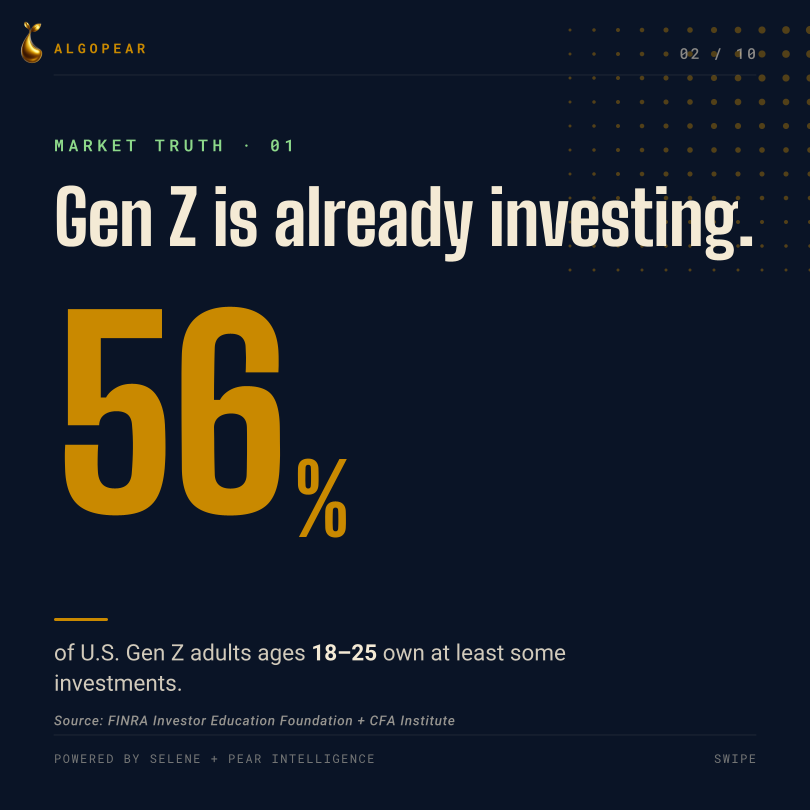

For years, the biggest banks genuinely believed they had time. Digital assets looked like a fad, retail investing apps felt like toys, and the idea that younger members would trust non-bank platforms seemed unrealistic. But the reality shifted quietly and aggressively. The next generation didn’t wait for traditional institutions to modernize — they simply moved on.

They opened investment accounts on their phones, bought digital assets before breakfast, and learned diversification and automation from apps, not advisors. Month after month, deposits drifted out of traditional accounts and into platforms built for growth rather than storage. And while the incumbents hesitated, fintechs captured both the attention and the momentum. In the end, the flip wasn’t driven by innovation or vision — it was driven by survival.

Members had already changed where they “live” financially.

Most new investment accounts opened in recent years didn’t come from bank branches; they came from mobile apps designed for speed, clarity, and immediate decision-making. Once someone adapts to that level of convenience, the old model becomes nearly impossible to return to. At the same time, regulators slowly began giving clearer signals. ETF approvals, institutional-grade custody, enhanced compliance rails, and maturing frameworks removed the fog that once made big banks nervous.

What once looked too “risky” quickly became too “risky to ignore.”

And beneath all of this sat an uncomfortable truth that every executive understood: once members build financial habits outside your ecosystem, you rarely get them back. That single realization accelerated the pivot. The narrative inside boardrooms shifted almost overnight from skepticism to urgency. What was once “we’re not touching digital assets” became “we cannot afford to be last.” The slowest, most conservative institutions in the country are now sprinting, not because they suddenly believe in the future — but because the behavior of their customers left them no alternative.

To put it simply, the flip happened because the market forced the following realities into the spotlight:

This is the turning point the entire industry is now waking up to — and it sets the stage for the shockwave hitting community FIs next.

What’s happening at the top of the industry always finds its way downstream, and community FIs are about to feel the impact faster than anyone expected. For years, credit unions and community banks could afford to move slowly because the largest institutions moved slowly. But that buffer is gone. When incumbents flip their position on digital assets, embedded investing, and modern member engagement tools, it resets the entire expectation framework for the everyday consumer.

Members don’t differentiate between “big bank capabilities” and “community FI capabilities” — they just expect the same level of access everywhere. And once those expectations rise, they don’t fall back down.

The truth is, credit unions have already been feeling the early symptoms. Member engagement is dipping. Younger generations are drifting toward fintech apps for anything involving investing, earning, yield, or real-time data. Deposits aren’t as sticky as they used to be, and the relationship advantage that credit unions once relied on is eroding simply because the digital experience isn’t keeping pace.

The wave hasn’t fully hit yet, but the tide is undeniably moving in the same direction big banks just validated. The message for community FIs is clear: your members are watching incumbents adopt modern tools, and they will expect you to match that progress.

This isn’t a distant threat — it’s happening right now. Members are becoming more fluent in investing. They’re learning the language of digital assets. They’re comparing the speed, transparency, and convenience of fintech experiences to the slower, legacy tools offered by traditional platforms. And when the biggest banks start to normalize the idea that investing and digital asset access should be embedded, always-on, and mobile-friendly, the baseline for what counts as “competitive” instantly rises.

To keep pace, community FIs will need to make strategic upgrades in three critical areas:

These aren’t optional upgrades — they are the new foundation of what a competitive financial institution will look like in the 2025–2030 landscape. The market is shifting around community FIs whether they move or not. But the FIs that choose to adapt quickly have a unique advantage: they can leapfrog legacy complexity and adopt modern solutions more efficiently than the giants. The challenge is real, but so is the opportunity. Credit unions that respond now will not only retain their members — they’ll grow, lead, and redefine what “community finance” means in the digital era.

Early adoption isn’t just about being first — it’s about giving your institution the breathing room to learn, experiment, and perfect. When community FIs adopt modern investing and digital asset tools early, they get time to test different features, gather real member data, understand actual behavior, and shape the solution alongside their fintech partners.

That learning curve is priceless.

It lets credit unions refine the experience, tailor it to their membership, and discover what truly resonates long before the rest of the market catches up. But when an institution waits until the last minute, it loses that flexibility. There’s no experimentation phase, no iteration cycle, and no time to figure out whether the first solution they choose will even stick.

Early adopters aren’t just ahead — they’re informed, prepared, and in control, with a solution that fits their members instead of one rushed under pressure.

This industry shift doesn’t just change which products community FIs need to offer — it fundamentally reshapes how they must think about digital strategy moving forward. Modern members aren’t evaluating institutions the way they did twenty years ago. They’re no longer choosing based purely on location, brand familiarity, or the feeling of community alone. They’re choosing based on the experience that helps them take action quickly, learn continuously, and grow financially with confidence. And if the digital experience your FI provides feels slower, more limited, or more rigid than what members see from big banks or fintech apps, the comparison happens instantly — and not in your favor.

A competitive digital strategy in this new era requires far more than an online banking portal or a mobile app with incremental updates. It requires embedded investing, simple digital asset pathways, personalized financial insights, and intelligent touchpoints that guide members in real time. It requires tools that don’t just show information — they help members make decisions. And most importantly, it requires a mindset shift: digital can no longer be treated as a technical project. It has to become the heart of the member relationship.

What this moment forces every community FI to recognize is that innovation is no longer a side initiative — it’s the operating system. The institutions that thrive in the next decade will build their strategy around rapid testing, continuous learning, and consistent iteration, rather than slow, multi-year digital roadmaps that lag behind member behavior. This means empowering digital teams with the flexibility to experiment, the insight to measure real engagement, and the autonomy to refine solutions based on what members actually respond to, not what internal assumptions dictate.

In practical terms, credit unions will need to strengthen several key areas:

The thread running through all of this is simple: digital isn’t a channel anymore — it’s the battleground of trust and relevance. It’s where the member relationship begins, where decisions are made, and where loyalty is earned or lost. And the institutions that embrace this reality now will not only keep pace — they’ll redefine what community finance looks like in the modern age.

Every signal in the market is pointing in the same direction. The biggest banks in America have flipped their stance, fintech adoption is accelerating, and member expectations are rising faster than most community FIs can update their digital roadmap. The shift is already underway — and the real question is whether credit unions will shape this next era or be forced to catch up later under pressure. Early adopters aren’t just ahead technologically; they’re ahead strategically. They get time to experiment, time to collect member data, time to refine solutions, and time to build a digital experience that actually fits their community instead of one rushed out of necessity.

This is exactly where AlgoPear and Selene Intelligence come in. We give community FIs the power to embed modern investing, digital asset education, real-time insights, and personalized financial intelligence directly into the experiences your members already use — without the multi-year lift or the heavy technical debt. It’s a platform built for agility, built for iteration, and built for credit unions that want to stay relevant as the market shifts around them. Instead of waiting for the pressure to mount, you can start learning today, start experimenting today, and start creating the kind of financial experience your members will expect everywhere tomorrow.

The institutions that act now will define the next chapter of community finance. They’ll retain deposits, elevate digital engagement, strengthen loyalty, and meet their members at the exact point where financial life is happening: in real time, inside the digital experience, with intelligence guiding every decision. The window of opportunity is wide open, but it won’t stay open long.

For credit unions ready to lead this shift — not chase it — the next step is simple.

Connect with a Selene Intelligence Luminary and see how this future becomes real for your members.

👉 algopear.com

.png)